Yahoo Movies

Yahoo Movies How Does Sleep Number's (NASDAQ:SNBR) P/E Compare To Its Industry, After The Share Price Drop?

Unfortunately for some shareholders, the Sleep Number (NASDAQ:SNBR) share price has dived 51% in the last thirty days. Indeed the recent decline has arguably caused some bitterness for shareholders who have held through the 47% drop over twelve months.

Assuming nothing else has changed, a lower share price makes a stock more attractive to potential buyers. While the market sentiment towards a stock is very changeable, in the long run, the share price will tend to move in the same direction as earnings per share. The implication here is that long term investors have an opportunity when expectations of a company are too low. Perhaps the simplest way to get a read on investors' expectations of a business is to look at its Price to Earnings Ratio (PE Ratio). A high P/E implies that investors have high expectations of what a company can achieve compared to a company with a low P/E ratio.

View our latest analysis for Sleep Number

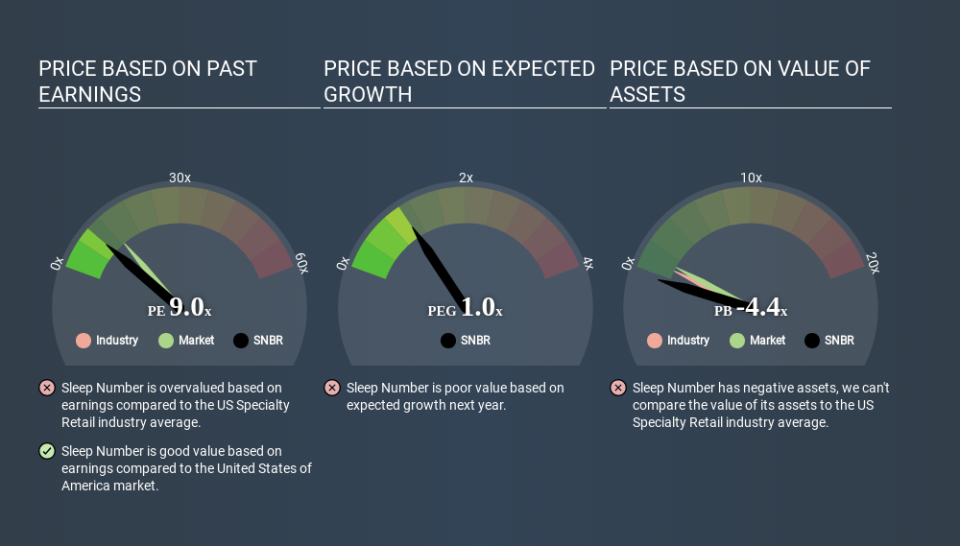

Does Sleep Number Have A Relatively High Or Low P/E For Its Industry?

Sleep Number has a P/E ratio of 9.02. As you can see below Sleep Number has a P/E ratio that is fairly close for the average for the specialty retail industry, which is 9.0.

That indicates that the market expects Sleep Number will perform roughly in line with other companies in its industry. If the company has better than average prospects, then the market might be underestimating it. Further research into factors such as insider buying and selling, could help you form your own view on whether that is likely.

How Growth Rates Impact P/E Ratios

Generally speaking the rate of earnings growth has a profound impact on a company's P/E multiple. Earnings growth means that in the future the 'E' will be higher. Therefore, even if you pay a high multiple of earnings now, that multiple will become lower in the future. And as that P/E ratio drops, the company will look cheap, unless its share price increases.

Sleep Number increased earnings per share by a whopping 41% last year. And its annual EPS growth rate over 5 years is 17%. So we'd generally expect it to have a relatively high P/E ratio.

Remember: P/E Ratios Don't Consider The Balance Sheet

It's important to note that the P/E ratio considers the market capitalization, not the enterprise value. Thus, the metric does not reflect cash or debt held by the company. In theory, a company can lower its future P/E ratio by using cash or debt to invest in growth.

Spending on growth might be good or bad a few years later, but the point is that the P/E ratio does not account for the option (or lack thereof).

So What Does Sleep Number's Balance Sheet Tell Us?

Net debt is 33% of Sleep Number's market cap. While that's enough to warrant consideration, it doesn't really concern us.

The Bottom Line On Sleep Number's P/E Ratio

Sleep Number's P/E is 9.0 which is below average (13.4) in the US market. The company hasn't stretched its balance sheet, and earnings growth was good last year. If the company can continue to grow earnings, then the current P/E may be unjustifiably low. Given Sleep Number's P/E ratio has declined from 18.5 to 9.0 in the last month, we know for sure that the market is more worried about the business today, than it was back then. For those who prefer to invest with the flow of momentum, that might be a bad sign, but for deep value investors this stock might justify some research.

When the market is wrong about a stock, it gives savvy investors an opportunity. As value investor Benjamin Graham famously said, 'In the short run, the market is a voting machine but in the long run, it is a weighing machine. So this free visual report on analyst forecasts could hold the key to an excellent investment decision.

Of course you might be able to find a better stock than Sleep Number. So you may wish to see this free collection of other companies that have grown earnings strongly.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.