Yahoo Movies

Yahoo Movies Does Aspen Aerogels (NYSE:ASPN) Have A Healthy Balance Sheet?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Aspen Aerogels, Inc. (NYSE:ASPN) does use debt in its business. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Aspen Aerogels

What Is Aspen Aerogels's Net Debt?

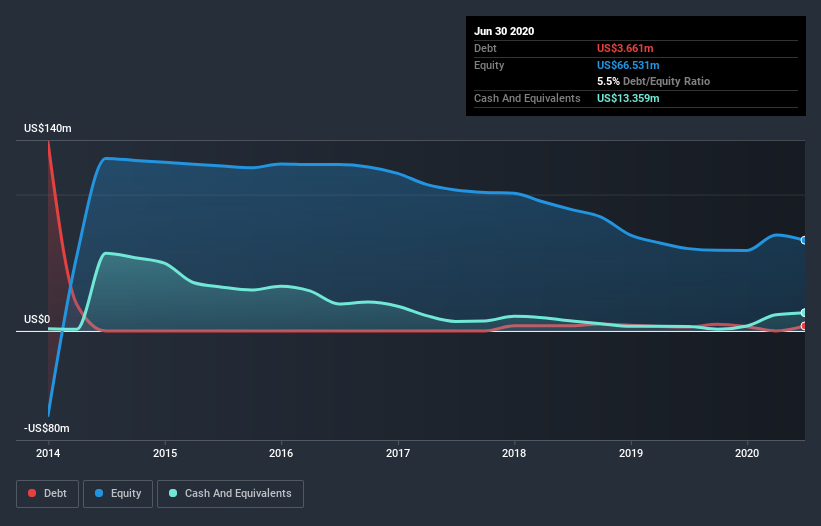

As you can see below, at the end of June 2020, Aspen Aerogels had US$3.66m of debt, up from US$2.89m a year ago. Click the image for more detail. However, it does have US$13.4m in cash offsetting this, leading to net cash of US$9.70m.

How Healthy Is Aspen Aerogels's Balance Sheet?

According to the last reported balance sheet, Aspen Aerogels had liabilities of US$13.3m due within 12 months, and liabilities of US$17.7m due beyond 12 months. On the other hand, it had cash of US$13.4m and US$19.2m worth of receivables due within a year. So it actually has US$1.51m more liquid assets than total liabilities.

Having regard to Aspen Aerogels's size, it seems that its liquid assets are well balanced with its total liabilities. So it's very unlikely that the US$300.9m company is short on cash, but still worth keeping an eye on the balance sheet. Succinctly put, Aspen Aerogels boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Aspen Aerogels's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Aspen Aerogels wasn't profitable at an EBIT level, but managed to grow its revenue by 15%, to US$135m. We usually like to see faster growth from unprofitable companies, but each to their own.

So How Risky Is Aspen Aerogels?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Aspen Aerogels had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of US$5.1m and booked a US$12m accounting loss. But the saving grace is the US$9.70m on the balance sheet. That means it could keep spending at its current rate for more than two years. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Take risks, for example - Aspen Aerogels has 2 warning signs we think you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.