Yahoo Movies

Yahoo Movies 'We are a broken people': The importance of Black homeownership and why the wealth gap is widening

If Robert York was ever bone tired, he didn’t show it.

After working two jobs, the father of 11 would return home to his North Lawndale two-flat greystone on Chicago’s West Side and hose down the chalk marks his kids made while playing on the porch.

The home was his prized possession. This was the early 1960s, and like most Black people in the neighborhood who were land contract buyers, York was paying dearly for it – and living in constant fear of losing his home.

Land contract buyers were on the hook for a down payment, high monthly payments and maintenance of the house while the deed remained in the seller’s name until the very last payment was made. A single missed payment was grounds for eviction.

Many working-class Black families in the 1950s and ’60s were forced to turn to speculative sellers after the federal government refused to insure mortgages in redlined African American neighborhoods.

Speculators often bought homes at a discount from white families as they fled racially changing neighborhoods to sell them months later to Black families at inflated prices and high interest rates.

In the 1950s and ’60s, 85% of Black families who bought a home in Chicago did so under a land installment contract, according to experts.

The same financial institutions that denied creditworthy Black buyers were happy to give mortgages to white speculators who then sold them to Black families for double or quadruple what they paid, says Beryl Satter, professor of history at Rutgers University and the author of "Family Properties: Race, Real Estate, and the Exploitation of Black Urban America."

Discriminatory lending practices, such as land contracts, often described as a "poor man's mortgage," were not the only barriers Black homebuyers faced historically. Decades of housing segregation, systemic denial of loans or insurance in predominantly minority areas and a persistent income gap have stood in the way of Black homeownership, curtailing their ability to build generational wealth.

More than half a century after the Fair Housing Act was signed into law in 1968, not only is the homeownership gap between white and Black Americans wider than it was in 1960, the homeownership rate of Black Americans is expected to be lower (40%) in 2040 than it was in 2020 (41%), according to a study by the Urban Institute, a Washington-based research organization focused on upward mobility and equity.

Though some of the structural and systemic issues may have been alleviated after the passage of the Fair Housing Act, issues including financial education and awareness can still limit homeownership for lower-income households (a disproportionate share of whom are Black and Hispanic) or trap them into exploitative transactions.

“The story of Black homeownership in the U.S. is a case where they get access and the access is wiped out, and then they get access and the access is wiped out,” Satter says. “So there's a cycle where African Americans get either no loans from mainstream banks, which push them into purchasing from scavengers and outlying speculators, or the pendulum swings the other way and they get loans that are official, but they are predatory also.”

For instance, in the decade leading up to the U.S. housing crash of 2008, many banks disproportionately targeted Black and Latino homeowners for sub-prime mortgages.

In 1968 – almost a decade after the Yorks bought their home on contract – a grassroots movement led to the establishment of the Contract Buyers League. The CBL used tactics such as picketing, payment strikes and even lawsuits to force many lenders to renegotiate predatory contracts.

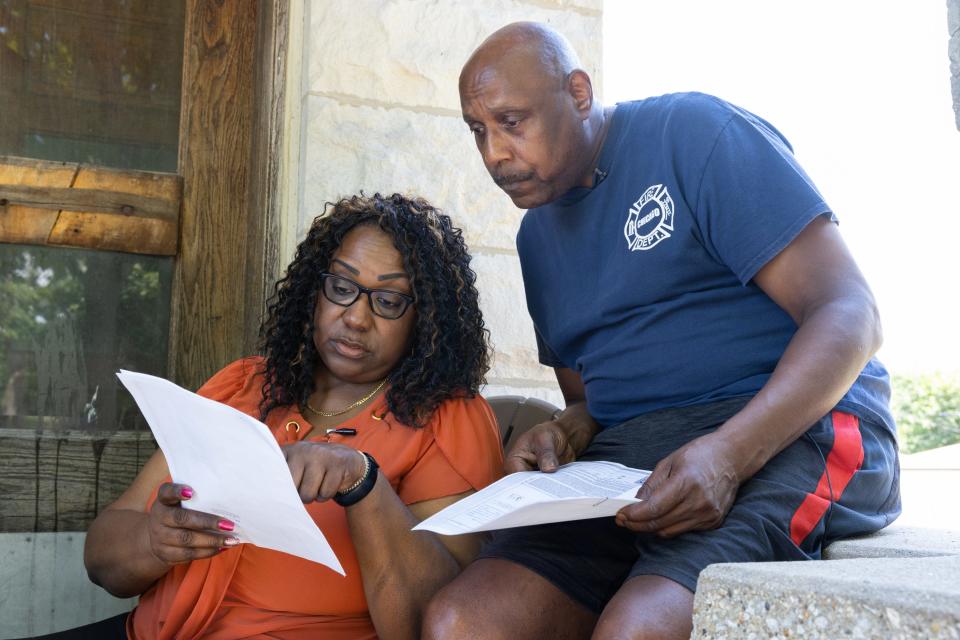

On a recent morning, siblings Donald and Sandra York sat on the same porch where they once drew the chalk designs, reflecting on the sacrifices their parents made to become homeowners.

To make ends meet, their mother, Ruby, worked as a midwife, a babysitter and a seamstress. The family of 13 crammed into one floor of the house, renting out the other to help make the monthly installment payments.

On some nights, Ruby went hungry, they said.

“Sometimes she went without so that we could have,” Sandra says. “She just made sure that all of us ate before she would even pick up a morsel, and whatever was left is what she had.”

She was the first on her block to attend CBL meetings and picket against the lenders, Sandra says.

Others, including their father, worried the protests could lead to eviction.

“She was the Muhammad Ali,” says Donald, 63, a retired Chicago firefighter. “She had that focus.”

The Yorks were one of the lucky families.

USA TODAY retrieved documents from the Cook County Clerk’s Office and the National Archives in Chicago that show the Yorks received the deed to their home in 1970 – 11 years after they "bought" the house.

USA TODAY found documentation that listed the Yorks as plaintiffs in a lawsuit in 1969, along with the Contract Buyers League.

More than 70 boxes that contain information on two lawsuits filed on behalf of contract buyers are housed at the archives.

The Yorks were among the contract buyers who withheld payment on their home, which was sold to them in 1959 for $23,000, according to documentation in the archives. According to Realtor.com, the house is worth $333,200.

The York siblings say they were shielded from many of the details by their parents and saw the deed document, as well as proof related to the lawsuit, for the first time.

“I can see them up there smiling,” Donald York says of his late parents. “You know, you guys can actually see now what we went through, and this is what happened to us.”

Donald, who lives in the York home, says it has served as a safety net for the siblings whenever they needed a place to get back on their feet.

From 2018-2020, while the overall homeownership gap between white and Black households was marked by a 30-percentage-point difference, the gap was much narrower for those with higher incomes and college education.

Among those earning $100,000-$149,000, the homeownership gap between white and Black households dropped to 15 percentage points; for those who earned $150,000 or more, the gap narrowed to 11 percentage points, with homeownership rates at 88% and 77% for white and Black households respectively, according to Urban Institute data.

Only 18% of Black households made $100,000 or more in 2019, according to an analysis by Pew Research.

Obtaining a mortgage in 1967

Marva Watkins, 81, who has owned four homes through the decades starting in 1967 on Chicago’s South Side, says Black people with a college education, good incomes and steady jobs have had access to financing and a shot at the American dream at least since the 1960s.

Watkins, who grew up in Cleveland, was raised in rental homes. Her mother was an elevator operator. Her father was a barber.

After graduating from the University of Chicago, where she met her husband, Watkins began working for the Social Security Administration. Her husband, four years her senior, also worked there.

In 1967, one year before the Fair Housing Act was enacted, Watkins, then 26, and her husband bought their first home in Avalon Park on Chicago’s South Side. They were the second Black family to move into the neighborhood. Today it is majority Black.

The couple bought the single-family home for $31,000 with a 20% down payment and a conventional mortgage from the First Federal Savings & Loan Association of Chicago. Their combined income was about $12,000, or about $106,000 in 2022 dollars.

“Neither of us really grew up in a house,” she says. “So one of the first things we did once we got married was just start saving to buy a home. And we were the first among our friends to buy one.”

Soon, most of her Black college friends also had bought homes.

Watkins and her husband had no problems qualifying for a mortgage, perhaps because they both had steady government jobs, she says.

In October 1981, they bought a second home for $180,000 in the Jackson Park Highlands in the South Shore community, borrowing $125,000 at an adjustable interest rate of 14.5%. A 30-year fixed mortgage rate in October 1981 was 18.2%, according to data from Freddie Mac.

SUBSCRIBE: Help support quality journalism like this.

By then, her husband was working as a management consultant after getting an MBA from the University of Chicago.

By 1990, Watkins sold the house for $325,000. Building equity in each home helped with the next purchase, she says. In 2008, she bought her fourth home, a condominium on the South Shore, for $340,000 in cash.

“The cost of living for me right now is low, I have no debt, and I'm still able to save money each month, which will benefit my children,” she says.

Several people in her extended family have had positive experiences with homebuying over the years, she says. USA TODAY spoke to three of them, all of whose older family members were part of the Great Migration from the South: Sidney Craddock from Philadelphia, Dorita Taylor of Peekskill, New York, and Nancy Hite-Norde, a real estate agent from New York.

With a little help from the FHA

Despite a history of racial discrimination in federal programs starting in the 1930s, Federal Housing Administration-backed loans and down-payment assistance programs have played an important role in recent years in assisting "creditworthy" borrowers who struggle to put down a 20% down payment, such as first-time homebuyers and homebuyers of color. A conventional mortgage typically calls for a minimum credit score of 620 (which is considered fair), but for FHA-backed loans, the requirement is only 580, making more people eligible for loans.

Sidney Craddock bought his first home in 2005 at age 53.

It was an $85,000 townhouse in the Germantown section of Philadelphia. As a first-time homebuyer, he qualified for an FHA loan through the Bank of America with a 30-year mortgage and a $5,000 down payment.

The sub-prime mortgage crisis was brewing, he says, and mortgage brokers tried to convince him to buy a more expensive home than he could afford.

“There are some crooked people out there. But I didn’t fall for that,” he says.

“I had a good credit score, and I didn’t overextend,” he says. “I got the mortgage fairly quickly.”

Because he thought he was late to the homebuying game, Craddock, who worked in janitorial service at a hospital, made higher monthly payments and paid off his loan in 13 years. The home has more than doubled in value, he says.

Three years ago, at age 66, he bought a second town house as an investment property for $180,000. He says maintaining a good credit score was key: As a first-time homebuyer, his credit score was 720. It is now 824, a nearly perfect score.

Buying that first home was “the best decision I made,” he says.

Why is Black homeownership important?

Dorita and Willie Taylor of Peekskill, New York, bought their first home in 1983 when they were in their early 30s. She was a nurse, and he worked in medical records.

They bought a town house for $64,000 with an FHA loan in a “mostly white enclave.”

“We easily qualified because we were both working,” Dorita says.

The town house was to be a starter home, but they stayed and raised three children. The house is worth more than four times what they paid, the couple estimate.

“It meant stability and a way of achieving the American dream,” she says. “We could also build some equity.”

She hopes to pass down the house to her kids.

Economists consider homeownership an effective way to build generational wealth, especially for low-income households.

In 2016, the median wealth of white families was $171,000, or 10 times that of Black households, whose median family wealth is $17,600, according to Pew Research.

Achieving the 'American dream'

Nancy Hite-Norde, 66, a real estate agent with Coldwell Banker in Westchester County, says the low homeownership rate among Black families is a good barometer of the treatment of Black people in this country.

Although those with strong credit scores and steady work history can buy a home regardless of race, it takes Black families longer to assemble those financial building blocks because of historical discrimination in employment, financing, greater college debt and disinvestment in majority-Black neighborhoods, she says.

“The desire to own a home is very strong in the Black community, but it takes them longer to build up the resources,” she says.

The lack of generational wealth is not limited to financing; it can also translate to a lack of generational wealth of knowledge and exposure.

People who grow up in homes, as she did, are exposed to discussions about mortgages and monthly payments that others probably are not.

“Because if you've lived in a home, you’ve probably seen your parents talk about what has to be done to pay the mortgage," she says.

Generational wealth and a lack of a safety net

Falling homeownership rates will make it harder for Black families to pass on wealth to future generations, says Janneke Ratcliffe, vice president of the Housing Finance Policy Center at the Urban Institute.

“It (homeownership) is a channel to funnel economic privilege and benefits to you through tax breaks and through appreciation,” Ratcliffe says. “Imagine the wealth generated simply by having a 2.5% mortgage for 30 years instead of a 5% or 6% mortgage over a lifetime."

That leaves many Black Americans experiencing a job loss during an economic downturn or looking for help on a down payment on their home, unable to turn to their families.

The 'plunder' of Black wealth and the Race Tax Model

Chicago played a central role in shaping federal policy in the 1930s, which contributed to redlining, says Bruce Orenstein, artist in residence at Duke University's Samuel DuBois Cook Center on Social Equity.

“The restrictive covenant template was developed here and was then exported around the country,” says Orenstein, who is working on a series about the history of housing segregation in Chicago.

Nathan MacChesney of the Chicago Plan Commission created the covenant in 1927 to make sure real estate agents didn't sell homes in white neighborhoods to Black buyers, Orenstein said.

From 1950-1970, Chicago’s Black community lost $3.2 billion to $4 billion because of racist policies and predatory housing contracts, according to a Duke University report in 2019 led by Orenstein.

The report, "The Plunder of Black Wealth in Chicago," calculated that African Americans purchasing on contract paid, on average, $587 more each month (in April 2019 dollars) than they would have had they paid the fair price for their home and had a conventional or FHA- backed mortgage. The report found that, on average, sellers marked up the cost of contract homes by 84%.

Orenstein says knowing this history is foundational to understanding how to remedy the damage done by a greater part of a century of racialized housing policy.

Based on the Yorks' contract information, Amber Hendley, one of the researchers on the report, created a Race Tax Model (buyer’s payment minus seller’s payment) for USA TODAY to show the premium paid by the Yorks, calculated using the price of the home, down payment and interest rates over a 25-year mortgage term, the most common term at the time.

The difference between what the Yorks agreed to pay over 25 years for a home they bought for $23,000 in 1959 and the seller's purchase price of $15,000 (obtained by the data set collected by the researchers) is $22,150 in 1959 or $157,814 in 2022 inflation-adjusted dollars.

The Great Recession and resurgence of land contracts

The past decade saw a resurgence in land installment contracts nationwide in the wake of the foreclosure crisis.

A high percentage of these properties are in African American neighborhoods, according to a paper by the Federal Reserve Bank of Atlanta.

Investors bought foreclosed homes when Fannie Mae and Freddie Mac began selling houses for as little as $10,000 each, often bundling them, says Sarah Bolling Mancini, a staff attorney focusing on foreclosures at the National Consumer Law Center.

“So investors were buying them in bulk, and they decided to sell them, quote-unquote, using a contract for deed or land contract,” says Mancini who co-wrote an NCLC paper titled “Toxic Transactions.” “In part, because that was the most advantageous way for that investor to sell that involved a very easy way of taking back the property if someone defaulted.”

About a dozen states require that land contracts be publicly recorded, an important provision that protects all parties involved by documenting the buyer’s homeownership, according to a study by the Pew Charitable Trusts.

Though it is difficult to determine its prevalence nationally, as most states don't require these transactions to be recorded, about 36 million Americans have used some form of alternative financing, a survey by Pew found.

'Devastating': A land contract in Detroit

Sonja Bonnett, a Detroit resident, has lived that reality.

After years of renting homes in not-so-great neighborhoods and dealing with "slumlords," the married mother of seven decided in 2011 to buy a home.

Bonnett, who worked as a waitress while her husband worked construction jobs, says they were never financially secure.

They’d lived in homes that "were falling apart," and they'd been evicted a couple of times. Her credit score was low, and she doubted she would qualify for a mortgage.

Most homes she saw needed extensive repairs, but she kept looking until she found one she thought she could work with. It was missing siding on one side and had no plumbing, “but the things that needed to be fixed in that home, my husband was able to fix,” Bonnett said.

The house, owned by an out-of-state investment company, was $50,000. The couple made a $2,500 down payment and had a monthly installment payment of about $600.

Things seemed to be going fine until two years later when a yellow bag was hung on her front door with a letter inside: “Detroit is notorious for hanging a yellow bag on your door when you are in danger of foreclosure or you're about to be foreclosed,” she says. “The letter said that the house was $5,000 behind in property taxes.”

When she contacted the investment company, she found that it had not paid property taxes for years on the house. The company sent her the deed.

“It was devastating. It might as well have been $5 million because we didn't have $5,000 in the bank or laying around,” she says. “We were living paycheck to paycheck.”

She found out that the investment company paid $1,100 for the property it sold her for $50,000.

“I think I was willfully ignorant about the process, willfully ignorant about how predatory it was,” she says. “A lot of people who do (buy via) land contracts in Detroit are in that same position. They don't care that it's gonna take them forever to pay it off. They don't care that the house is not worth (it). Their whole thought is that American dream thing: Oh, I'm going to be a homeowner, and I don't have to pay rent anymore.”

She continued living in the house during the foreclosure proceedings. A few more foreclosures in the neighborhood and an increase in gang activity made living there more dangerous.

Bonnett approached a housing nonprofit for assistance but was not eligible because she was a land contract buyer. The nonprofit referred her to Bernadette Atuahene, a professor at Chicago-Kent College of Law.

“She ended up educating me on the fact that not only was I losing my home illegally, essentially because the city had over-assessed my house at that time, the house was worth $5,000, maybe," Bonnett says. “And the city had assessed it as something like $25,000.”

Bonnett says she decided to partner with a nonprofit to spread awareness among other Black homeowners in Detroit and worked with community organizations that purchased homes to show the city what was possible.

The community organization bought three homes for residents who had illegally lost their homes.

The timing worked out for Bonnett. The nonprofit helped her move into one of the homes before her foreclosure was complete.

She serves as a community legal advocate for the Detroit Justice Center.

“My first mission is to educate the community about the programs that are available and about how people can be proactive about the appeal process in Detroit,” she says.

Homeownership: A 'bucket list' item

When Robert and Ruby York moved into the North Lawndale house, the couple and their children were forced to live in the basement for an entire year, while the white sellers lived on the upper level – rent-free.

"The white family just refused to leave," says Sandra York, who works as a paralegal. "They also made sure to use up all the oil (heating oil) in the drums before they left. They didn't want to leave anything behind for the Black family."

The house, which their parents bought under contract in 1959, sits a few blocks away from where, seven years later, in 1966, Martin Luther King Jr. moved – and brought attention to the poor living conditions of Black families on the West Side of Chicago.

The York family achieved the American dream of homeownership, and Sandra and Donald have owned multiple homes over the years.

"It's part of your bucket list," Donald says. "It's what my parents expected after all their sacrifices."

Neither encountered any barriers to homeownership when they bought homes in the 1990s and early 2000s.

“My wife was a teacher, and I was in the fire department, and it was like, ‘Come on down,’” Donald says.

Asked why they think the Black homeownership gap persists, Sandra says:

"There's no sugar-coating it. We are a broken people because we've been on the ground with knees on our necks for generations and to try and come back from that. When you're pounded on and you're pounded on and you're pounded on, somewhere along the line, you lose a little bit of faith and a little bit of hope."

Swapna Venugopal Ramaswamy is a housing and economy correspondent for USA TODAY. You can follow her on Twitter @SwapnaVenugopal and sign up for our Daily Money newsletter here.