Yahoo Movies

Yahoo Movies Hut 8 Mining Corp. (TSE:HUT) Analysts Just Slashed This Year's Estimates

The analysts covering Hut 8 Mining Corp. (TSE:HUT) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. Revenue and earnings per share (EPS) forecasts were both revised downwards, with analysts seeing grey clouds on the horizon. Surprisingly the share price has been buoyant, rising 46% to CA$4.51 in the past 7 days. Whether the downgrade will have a negative impact on demand for shares is yet to be seen.

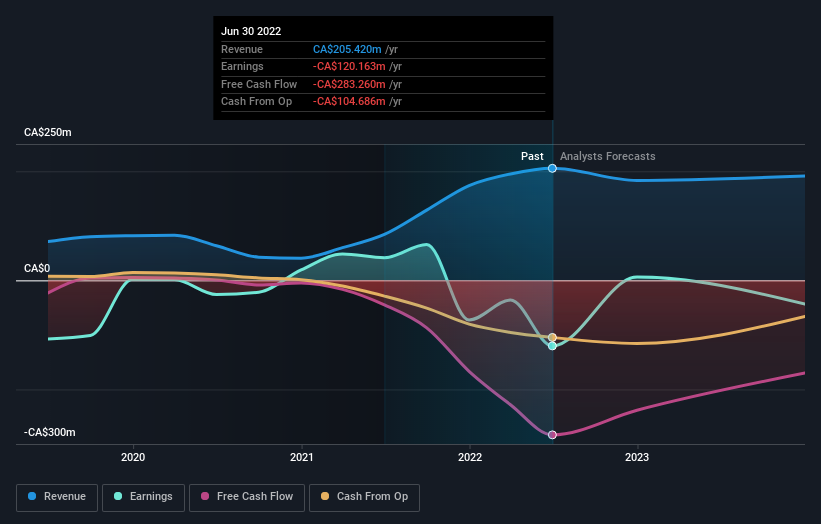

Following the downgrade, the consensus from three analysts covering Hut 8 Mining is for revenues of CA$183m in 2022, implying a definite 11% decline in sales compared to the last 12 months. Losses are predicted to fall substantially, shrinking 89% to CA$0.065. Before this latest update, the analysts had been forecasting revenues of CA$227m and earnings per share (EPS) of CA$0.38 in 2022. So we can see that the consensus has become notably more bearish on Hut 8 Mining's outlook with these numbers, making a measurable cut to this year's revenue estimates. Furthermore, they expect the business to be loss-making this year, compared to their previous forecasts of a profit.

View our latest analysis for Hut 8 Mining

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 20% by the end of 2022. This indicates a significant reduction from annual growth of 42% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 18% per year. It's pretty clear that Hut 8 Mining's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The biggest low-light for us was that the forecasts for Hut 8 Mining dropped from profits to a loss this year. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that Hut 8 Mining's revenues are expected to grow slower than the wider market. Given the serious cut to this year's outlook, it's clear that analysts have turned more bearish on Hut 8 Mining, and we wouldn't blame shareholders for feeling a little more cautious themselves.

So things certainly aren't looking great, and you should also know that we've spotted some potential warning signs with Hut 8 Mining, including recent substantial insider selling. For more information, you can click here to discover this and the 4 other flags we've identified.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here